This year’s Swiss real estate fair IMMO25 took place from January 15-16. Novalytica was represented with a stand and thus had the opportunity to present its diverse range of data products and services to over 5,000 visitors. This year’s focus was on the topic of ESG reporting:

- The co2lect application for smart collection and management of consumption data: Read more

- Our support in the preparation of all relevant data for various reporting standards, benchmarks and certificates: Read more

- Alphaprop, our data portal that contains all published ESG KPIs of the Swiss indirect investment universe to compare products with each other and with benchmarks: Read more

Two panel discussions in front of a full audience and many exciting conversations with familiar and new faces characterized the two days of the trade fair.

From data flood to data insights – a new approach to ESG reporting

With the new regulatory requirements, a bunch of ESG KPIs must be reported. How do you escape this flood of data and generate insights with added value, for example a reduction path? At the panel discussion, various stakeholders discussed the regulatory development, the role of standards for comparability and the importance of a data strategy for the collection and processing of ESG data.

Thomas Spycher from Novalytica and Alphaprop introduced the topic and pointed out that practically all products in the area of indirect real estate investments now publish the environmentally relevant KPIs defined by AMAS/KGAST. He also pointed out that, in addition to the AMAS/KGAST requirements, there are a large number of benchmarks and certificates that are much broader in scope and require more data. In addition, benchmarks have changed over time and with them the requirements.

In the subsequent discussion, Massimo Mannino, CEO of Novalytica, Niklas Naehrig, Head of Consulting & Sustainability at Wincasa, and Elvira Bieri, CEO of SSREI, discussed the topic.

The discussion highlighted how difficult it is to obtain basic data such as energy consumption. This requires technical innovation, as consumption bills are often the only source of data. Novalytica has developed an AI-based algorithm that can automatically read invoices as PDFs or PDF scans and extract the data. This also takes into account the very broad and diverse energy provider landscape in Switzerland.

Another challenge that was mentioned was data quality, the requirements of which are becoming increasingly stringent. This requires a combination of intelligent algorithms and human expertise to ensure the completeness and plausibility of the data. Data collection is the first and most critical step in ESG data management. Only when all the necessary data has been properly recorded and is of high quality can it be linked together and used as a basis for calculating KPIs, e.g. in accordance with AMAS/KGAST.

Although data on the consumption of properties forms the baseline of many benchmarks and reporting standards, comprehensive ESG reporting requires additional dimensions, such as biodiversity, density of use or social and economic issues. These are covered by the SSREI as a comprehensive standard for sustainable real estate valuation.

In addition to calculating ESG KPIs for regulatory requirements and investors, the comparison with a benchmark is also of interest. Using the data collected by Alphaprop from the annual reports of real estate funds, investment foundations and listed real estate companies, a portfolio can be compared with a peer group. An owner can also benchmark himself against other SSREI participants within the SSREI. However, methodological comparability is primordial for a meaningful analysis, according to the discussion participants. Within the SSREI benchmark, this is provided by its own standard. The REIDA methodology has established itself as the standard for calculating environmentally relevant key figures in annual reports, which has greatly improved methodological comparability in recent times. However, there are still differences in the collection and processing of raw data.

The experts estimated that, in addition to the transparent reporting of the status quo, the focus will increasingly shift to concrete action plans such as a CO2 reduction pathway. In addition, the even greater spread of a standardized methodology for collecting, processing and calculating data was mentioned. This is also in view of the fact that disclosure is increasingly becoming a regulatory requirement, as is now the case in the EU with the CSRD.

Panel contribution

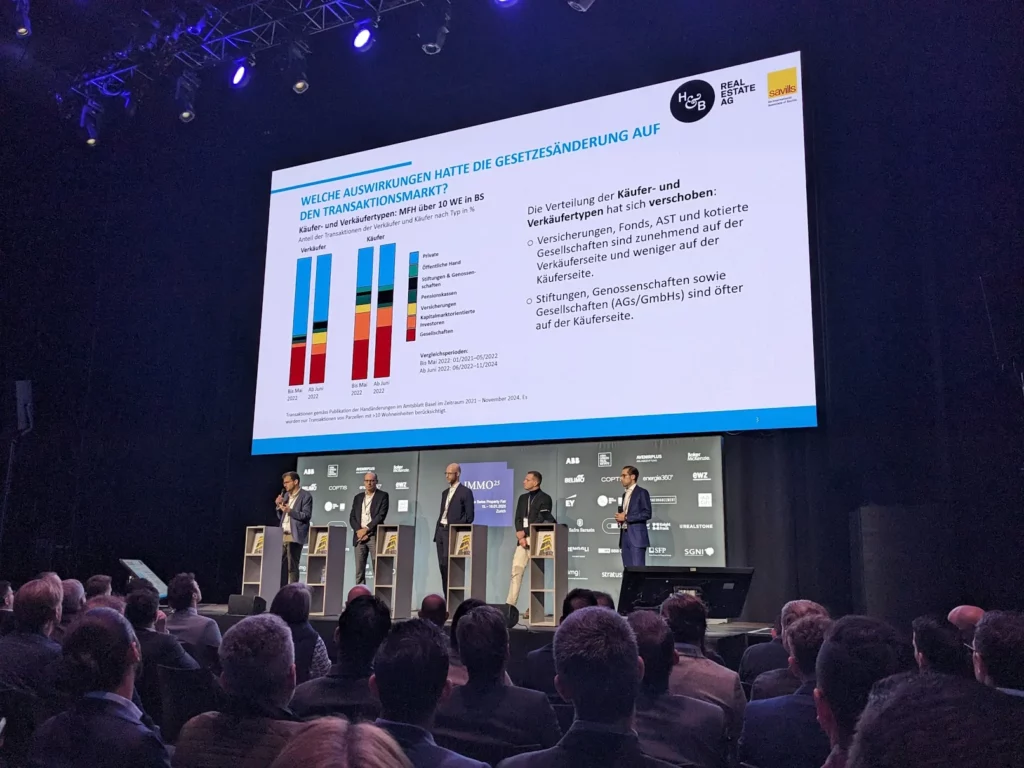

Development of the transaction market in Basel-Stadt since the adoption of the Housing Promotion Act

The current market study by H&B Real Estate examines the effects of the Housing Promotion Act on the transaction market in Basel-Stadt. Alphaprop was able to contribute its expertise in the collection and analysis of data. The study and its key findings were presented to the public for the first time at IMMO25.

The transaction market in the canton of Basel-Stadt remained active from 2022 to 2024, despite changes in the legal framework. The majority of property owners surveyed in Basel have kept their allocation in Basel stable across all types of use. However, an above-average 36% of investors have reduced their residential allocation since the revised Housing Promotion Act came into force. Institutional investors such as insurance companies, real estate funds, investment foundations and listed real estate companies are increasingly acting as sellers and less frequently as buyers. On the buyer side, however, foundations, cooperatives and companies (AGs/GmbHs) have significantly increased their share in the last two years.

This market shift could be due to both the new regulations and the turnaround in interest rates – however, it is difficult to clearly separate the influencing factors. The decline in market activity by certain players has already had an impact on real estate prices. Apartment buildings in the city of Basel are around 50 to 100 basis points below comparable properties in other cities. This finding has been confirmed in various transactions that have taken place.

For 2025, over a third of the investors surveyed are planning a further reduction in the residential allocation in Basel-Stadt. This trend is less pronounced for commercial properties. Only a small minority of the companies surveyed plan to increase their investment volume in Basel-Stadt. Over two thirds of respondents expect a slight (5%) or significant (10%) reduction in willingness to pay for residential properties in Basel-Stadt in 2025. A declining willingness to pay is also forecast for other types of use, albeit to a lesser extent.

The survey of relevant players in the Basel real estate market shows that the mood in the residential sector in particular remains gloomy, even two years after the change in the law, and that less capital is being allocated to the residential market in the canton of Basel City (purchase and construction).

Panel contribution